Bonds are money-borrowing instruments used by the issuer. We often borrow money from family, friends, and relatives. In the case of bonds, federal governments, municipalities, and corporate houses borrow money by issuing bonds, with the promise of an assured return to the bondholder in terms of a fixed interest rate at a regular interval (generally twice a year) and the principal amount on maturity of bonds. Depending on who the issuer is, bonds are categorized into three main types.

Types of Bonds

- Government bonds or T – bonds are the most trusted as the government is the guarantor. These are issued by the U.S. government with minimum risk of default. With less risk involved, government do not offer higher rates to the bondholders, which makes it less attractive for the public as an investment avenue.

- Municipal bonds are issued at the municipality level, state governments, or local governments. These are issued as fund-collecting instruments by local governments to finance public goods like physical or social infrastructure. In return, bondholders get a promised return as the interest rate and the principal amount on maturity.

- Corporate bonds are issued by big corporate houses. As corporate bonds have an inherent risk of default, they offer higher rates of interest to attract investment from the public.

Investing in bonds depends upon the quality of bonds. Commoners can get a sense of the quality of bonds by ratings from the Credit Rating Agencies (CRA) like Moody’s, Fitch, and Standard & Poor (S&P). Bonds may be rated as any of these – AAA, AA+, AA, AA-, A+, A, A-, BBB+, BBB, BBB-. These ratings are in descending order of quality, with the best bond rated as AAA and the poorest bond quality with a higher risk of default or junk are rated as BBB-.

Before investing in Bonds, investors must look into the risks associated with an investment in bonds.

Risks with Bond markets:

- Inflationary risk with bonds is a major risk. This is because, although returns on bonds are fixed in terms of interest rates, it may often fall short of price rise in the economy, with inflation exceeding the rate of interest on bonds. Bonds with longer maturity tenure may not keep pace with inflation.

- Credit risk is the risk associated with the ability of issuers to make timely payments on promised returns to their bondholders. Federal or municipal bonds have the lowest credit risk. Corporate bonds run high credit risk.

- Interest rate risk is important only when bondholders decide to sell their bonds before maturity. Bond price is inversely related to interest rates. A higher interest rate causes bond prices to fall. If bondholders intend to sell their holdings before maturity, they may have to settle for a lower price of bonds, if the interest rate in the bond market has risen. As bonds come with fixed interest rate return, and interest rate rises due to changes in the economy, new bonds become more attractive than earlier bonds, therefore old bonds are sold at a lower price.

A good retirement portfolio should have a spread between Treasury bonds and good quality corporate bonds. As returns on municipal bonds are tax-free, this makes them a lucrative portfolio component for individuals who fall in the high tax bracket. Bonds can be purchased either directly from the Feds or through a broker. Brokers charge commission for their service, it, therefore, makes sense to skip intermediaries.

Investors often face a dilemma of whether to invest in long-term bonds or short-term bonds. Long-term bonds offer higher interest rates compared to short-term bonds. But long term bonds carry inflationary risk, as the fixed return promised may not be sufficient enough to beat price rise in the economy. Long-term bonds also carry interest rate risks, as a higher interest rate in the bond market makes existing bonds less attractive in terms of the bond price. Medium-term bonds – 10-year bonds – should serve the purpose of investors, as it has features of both long-term and short-term bonds. It is long enough in terms of offering higher interest rates and short enough to face the risk of volatility in bond price.

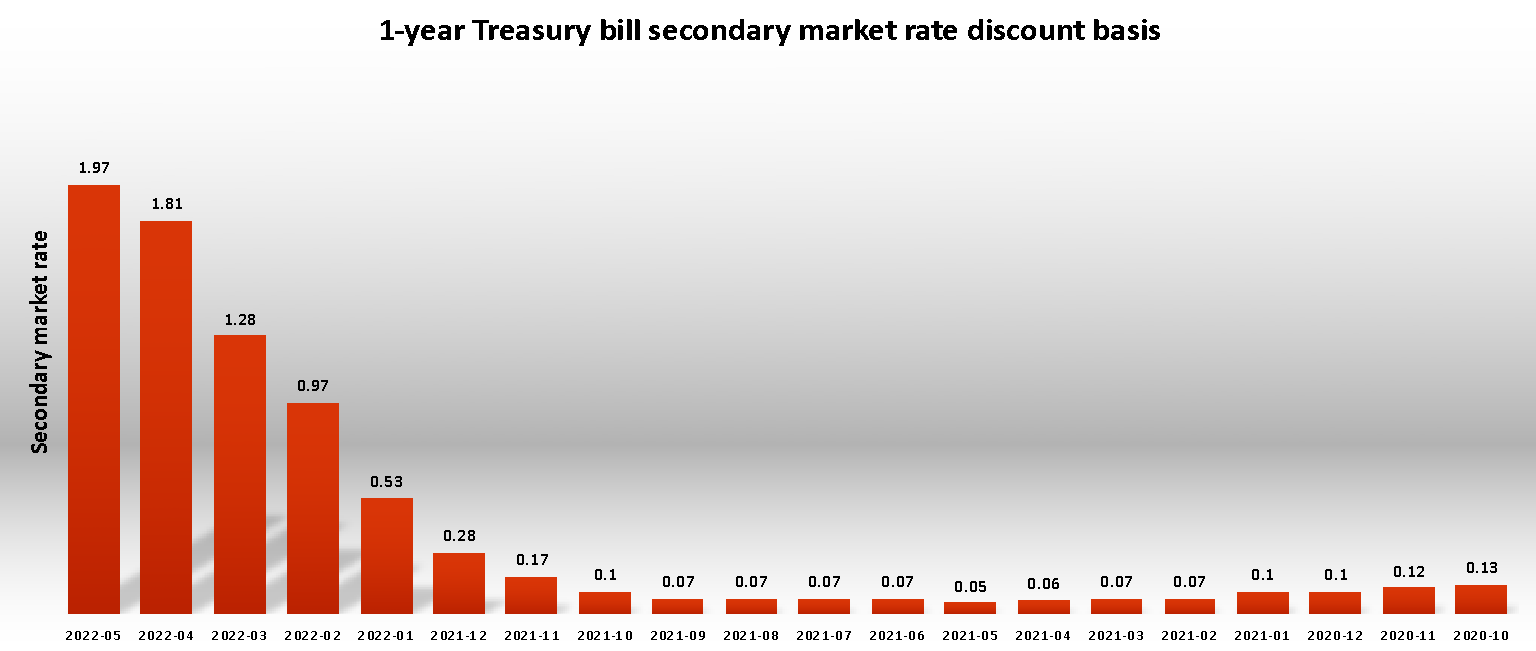

It is important for investors to get an idea about T – bills rate of return. The graph below shows the rate of return on a 1-year Treasury bill secondary market rate discount basis. It can be seen that in the last two years, the return has jumped by more than fifteen times, from 0.13 percent per year in October 2020 to 1.97 percent per year in May 2022. For information, the inflation rate in the U.S., the annual inflation rate for the months ended April 2022 is 8.3 percent.

Source: Federal Reserve Bank

A look at treasury bills with a maturity tenure of over 10 years shows that the return has been negative most of the time. Only recently, the rate of return is positive since April 2022. Long-term interest has clearly not kept pace with the rate of inflation in the economy.

Source: Federal Reserve Bank

Conclusion

Bonds are instruments of borrowing funds by governments and corporate houses in exchange for promised rate of return on borrowed funds. Government bonds have low credit risk but high interest and inflationary risk. Corporate bonds, on the other hand, has high credit risk. Individuals falling in higher tax brackets should invest in municipal bonds as returns from municipal bonds are tax-free. Return on government bonds falls short of covering inflationary risk, as is evident from the graphs. One must carefully do a cost-benefit analysis before investing in bonds as risk and return desirability differ from person to person. Young individuals with high-risk capacity should invest in stocks. Elderly people might find bonds lucrative in terms of low risk and higher stability. Ratings from Credit Agencies are helpful for selecting a good quality bond with low default risk, in case an individual would like to go for corporate bonds, which generally have high credit risk. Investors must stay away from bonds with poor ratings from Credit Rating Agencies.