Recession: Macroeconomic foundation to the global impact

As per the National Bureau of Economic Research (NBER), a Recession is “a significant decline in economic activity that is spread across the economy and lasts more than a few months”. It is a naturally occurring phenomenon mostly related to the business cycle of boom and bust. Strong economic growth is often accompanied by unwanted exuberance and overly confident economic sentiment causing malinvestments and other business errors based on the incorrect market expectations. It is important to know business cycle theory in order to understand the reason behind recession and recovery. A passing reference to three business cycle theories is made in the article without getting into much detail.

- Schumpeter’s Business Cycle Theory: Innovation is often related to the applications of a new invention to actual productions. It is the commercial exploitation of inventions through agents called ‘entrepreneurs’ who are innovators. Entrepreneurs gather in ‘swarm–like’ clusters to exploit the commercial opportunity of inventions. They are facilitated by the easy credit policy of financial institutions. Two phenomena are simultaneously at work – firstly, immense business opportunity attracts numerous entrepreneurs leading to an excessive supply of goods and services causing prices to fall and fall in profit opportunities. Secondly, easy credit policy by financial institutions causes factor prices to rise and rise in the cost of production. New innovations cease to exist and this marks the beginning of a recession.

- Keynes Theory of Business Cycle: Keyes explains recession through a fall in the marginal efficiency of capital (MEC). MEC is the profit expected from new investments. Profit expectations guide entrepreneurial activity. Higher the MEC, higher the profit expectations causing higher employment of labor and capital leading to a high level of output and production. Excessive output in turn lowers profit expectations. On the other hand, High employment causes shortages of labor and raw materials. Soon, business optimism gives way to skepticism and is finally replaced by market pessimism.

- Hawtrey’s Theory of Business Cycle: According to Hawtrey, monetary phenomenon lies at the core of any trade cycle. When banks have excess reserves with them, they become a bit less vigilant and pursue an easy money policy while lending to entrepreneurs and business houses. Easy credit induces producers to employ more labor and capital causing income and output to rise with subsequent increases in demand enticing producers to supply more goods and services. Meanwhile, banks realize that they have reached a dangerously low level of reserves and start calling back their loans and credits extended to business houses and entrepreneurs. This leads to a cut in credit supply and recovery of loans ensuing in a forced contraction in the economy which becomes self-fulfilling and causes cumulative restrictions on credit and layoffs by firms.

The above theories suggest, in a nutshell, that monetary phenomenon and wrong market incoherent expectations are the root cause of bust in the economy and are often the most important reason behind the economic recession. Figuratively, the expansion and contraction look like as shown below.

Economic expansion reaches a peak, followed by recession and then by depression similar to the ‘The great depression’ between 1929 and 1939. The bottom-most cycle is the trough. After the cycle reaches a trough, a ray of optimism sets in leading toward economic recovery and then begins the phase of economic expansion. The cycle continues. Having explained the theoretical foundations of booms and busts in the economy, let us proceed to the history of economic recession globally, with a specific focus on the USA.

History of economic recession

As per the Prospects Group (The World Bank), four global recessions ensued in the past even decades. These recessions coincided with a recession in the United States but not every recession in the United States coincided with a global recession. The four global recession is discussed below, with causes unique to each recession, but the underlying economic factor bears a striking resemblance.

- 1975 global recession was caused mainly due to a supply shock from the Arab oil one-year embargo that started in 1973 and ended in 1974. This led to a substantial rise in oil prices and triggered sharp inflationary pressure and a decline in growth in several countries. The period of stagflation lasted for the next five years.

- The 1982 global recession was caused by a series of events coming together in the form of the second oil shock in 1979, the Latin American debt crisis. A tight money policy was followed by the United States and other advanced economies and the following years witnessed sharp inflation, a fall in commodity prices, and an increase in global interest rates. Weak global growth and rising interest rates made it difficult for many Latin American countries to service their debts. A debt crisis soon engulfed the region.

- 1991 global recession was triggered by the gulf war and increased geopolitical uncertainty. The Gulf war led to a spike in oil prices. Parallelly, US lending institutions were witnessing widespread weakness, which impacted housing prices. The European Monetary System faced problems related to the exchange rate mechanism in 1992, and several member countries faced declines in their economic activity.

- The 2009 global recession is the worst financial crisis since the Great Depression. Loose regulations and supervision of financial markets and institutions, credit booms facilitated by high-risk lending in the U.S. mortgage markets were a precursor to the crisis in 2009. The immediate trigger was the collapse of Lehman Brothers in 2008. A high level of financial interconnectedness between the U.S. and other markets engulfed the global market in the crisis. European countries witnessed a severe Banking crisis leading to the financial crisis in 2011 – 13.

Causes of recession or slowdown in the global economy

Decades ago, a slowdown could be tracked emanating mainly from developed economies. But the scenario has changed in the present global context. Global recessions is better understood with a greater role of developing economies in Asia and emerging markets like China and India. So, in a way, monitoring cyclical fluctuations in advanced economies may not be sufficient enough to understand the global business cycle. Secondly, globalization and interlinkages of the market have dispersed the business cycle to a much global economy, which was earlier majorly restricted to the advanced economies.

The history of global recession shows that it was mostly caused either due to war, supply shocks, or monetary imbalance. The visible impact of a full-blown war is manifested in the form of loss of life and livelihood with a complete halt in economic activity in the war zone and nearby areas. The impact of war propagates to the economic sphere in the form of restricted trade, a halt in production, and hampered financial interlinkages with an obvious impact on reduced supplies. Shortage of production causes supply-push inflationary pressure on commodities and necessities like food, fuel, and edibles. The recent Ukraine war has clearly inflated food prices. However, fuel prices have artificially been kept lower by economic stakeholders in the war. It has prevented a full-blown and impending full-blown economic slowdown. It should be noted that the global economy had somehow recovered from the COVID pandemic. The spread of coronavirus had disrupted the global supply chain drastically with a sharp dip in economic sentiments. The marginal efficiency of capital (MEC) is bound to take a hit in such a scenario. As per the Keynes theory of business cycle, a fall in the marginal efficiency of capital leads to pessimism, and economic sentiments nose dives leading to slowdown and recession.

The second most important cause of recession is oil supply shocks, which may have been caused due to various factors similar to the gulf war, cartelization of OPEC production through which production of oil is kept artificially low, and economic sanctions imposed by developed countries. Oil price is often seen as the barometer of economic activity. Economic activity is directly related to oil price to a certain level. A sudden fall in oil price is regarded as a precursor to a slowdown in economic activity. An uptick in oil prices shows a recovery in global demand caused by progression in production and consumption. However, oil shocks causing a sharp rise in oil prices are also one of the reasons for the slowdown as oil is the lubricant of all economic activity. Increased oil price is inflationary and causes an overall increase in global commodity prices via an increase in transportation costs. Oil is a raw input factor in many production activities such as petrol and diesel, jet fuels, plastics, cooking gas, etc. Higher inflation level results in laborers seeking higher compensation in the form of wages. Recent reports show that inflation in the U.S. reached 9.1 percent in the month of June 2022, the highest inflation level in the last 41 years. A visible and prominent impact on the US stock market can be seen, as the result of a high level of inflation in the economy.

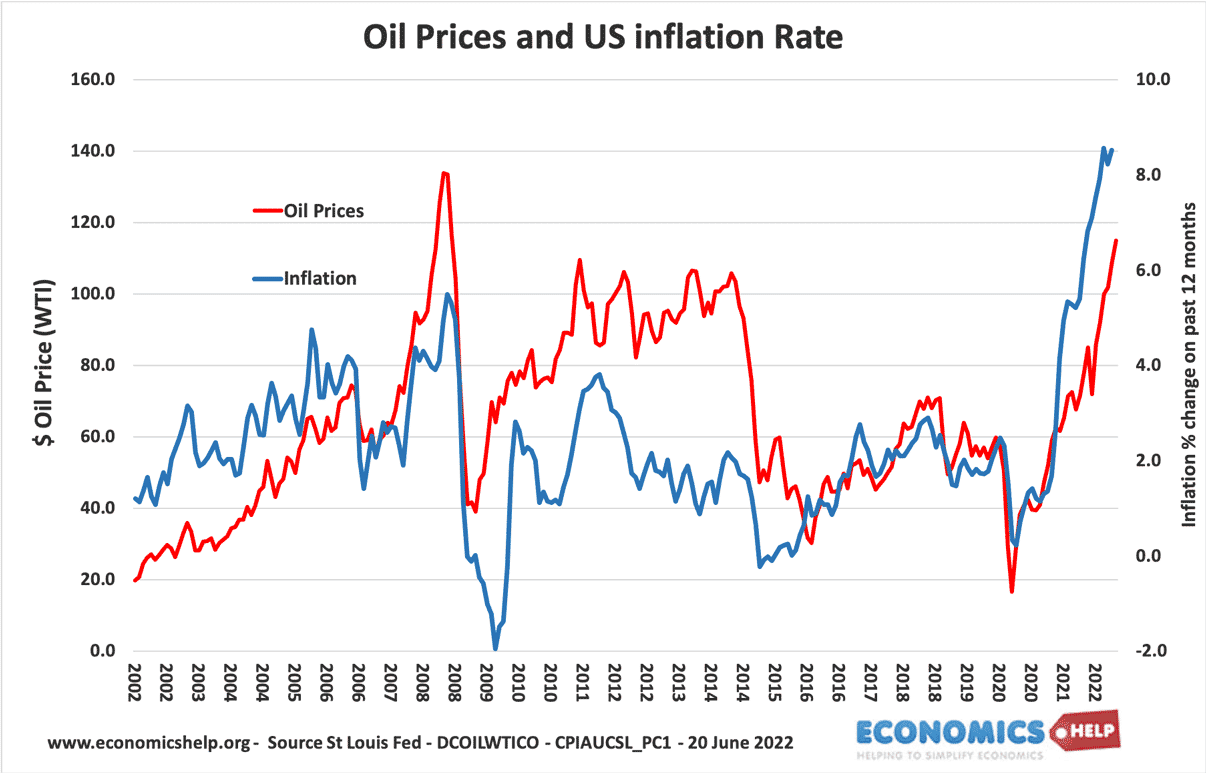

Source: St Louis Fed

As per an estimate by St Louis Fed, there is a low correlation of 0.27 between oil prices and inflation in the US. However, in parts, the phase of high oil price is followed by a higher level of inflation as can be seen between 2007 and 2008. Similarly, from 2020 onwards, spells of high oil prices have caused a higher consumer price index.

Another important cause of economic slowdown or recession is a loose monetary policy resulting in reckless spending, granting loans without collateral popularly known as credit booms, or excess money supply in the economy leading to uncontrolled inflation. The recession in 2008-09 is an important episode in the study of the global recession caused by loose monetary policy. Low-interest rate of 1% forced fixed-income investors to look for alternatives option for investments. Housing provided that lucrative opportunity to investors, and investment banks started providing bare loans to investors. These loans were high-risk loans that were casually backed by real assets. This led to a credit boom in the market, creating the US housing bubble that was bound to burst. The collapse of a major investment bank, Lehman Brothers was the immediate trigger that engulfed the entire global economy and developed into a full-fledged international banking crisis. The subprime lending crisis of 2008 vindicated Hawtrey’s business cycle theory which states that monetary phenomenon lies at the core of any business cycle.

Conclusion

The article discussed the cause of the global recession and focused on the US economy. Spells of economic slowdown or recession were backed by business cycle theories. Schumpeter’s Business Cycle Theory emphasizes the importance of innovation and entrepreneurship for continued growth. When new innovations cease to exist, the economy may fall into recession. However, history of the global economy has never witnessed any recession exclusively due to a lack of innovation. Keynes’s business cycle theory attributes the economic slowdown to the falling marginal efficiency of capital. However, a fall in MEC is often a result of other preliminary factors like economic shocks. Hawtrey’s business cycle theory puts the onus of recession on the imbalance in the monetary approach. Easy money policy and high-risk lending cause an imbalance in the supply and demand of money. The 2008 subprime crisis is a classic case vindicating Hawtrey’s business cycle theory.

Follow us on Instagram @InvestoCentral for financial content and investment tips.